Inventory management in HVAC accounting is the practice of tracking, valuing, and integrating parts and materials within your accounting system to produce accurate job costs, reliable financial statements, and real control over profitability. The industry term for this discipline is inventory accounting, and it sits at the intersection of field operations and financial reporting. Most HVAC owners understand what is inventory management in HVAC accounting at a surface level, but few connect it deeply enough to their books to see where margin actually disappears. ServiceTitan defines HVAC inventory management as ordering, paying for, and storing items technicians need, with tracking, asset management, forecasting, and vendor management as core components. When those operational activities feed directly into your accounting records, you gain the financial clarity that separates profitable HVAC businesses from ones that stay busy but never seem to get ahead.

What is inventory management in HVAC accounting?

HVAC inventory accounting covers two parallel tracks: the operational side and the financial side. Both must work together for your numbers to mean anything.

The operational side: what you track

On the operational side, HVAC inventory control means knowing exactly where every part and material sits at any moment. That includes stock in your warehouse, parts loaded on service trucks, and materials staged at a job site. The moment a technician pulls a capacitor off a truck to complete a repair, that movement needs to register somewhere. Without that registration, your inventory balance is fiction.

The key operational processes are:

- Ordering and receiving: Creating purchase orders, receiving deliveries, and confirming quantities match what was invoiced

- Storage and location tracking: Knowing whether stock is in the warehouse, on a specific truck, or at a job site

- Status management: Marking inventory as available, on hold, in use, or billed

- Demand forecasting: Using historical job data to predict what parts you will need before peak seasons hit

- Vendor management: Maintaining supplier relationships, tracking lead times, and managing returns or warranty claims

ServiceTitan’s inventory platform automates these status changes, moving inventory from “available” to “on hold” to “used” and triggering replenishment orders based on actual usage. That automation closes the gap between what your field team does and what your accounting records show.

The accounting side: how costs flow

On the accounting side, every inventory movement must produce a financial transaction. When you purchase parts, you capitalize the cost to an inventory asset account. When a technician uses those parts on a job, the cost moves out of inventory and into Cost of Goods Sold or a Work in Progress account tied to that specific job. This flow is what makes job costing accurate.

HVAC accounting works best when every inventory movement, whether a pull, transfer, or usage, triggers an accounting transaction that moves costs into job-specific WIP or expense accounts. That transaction chain is what gives you precise gross margin data by job, by technician, or by service type.

Pro Tip: Set up separate inventory sub-accounts in QuickBooks for warehouse stock, truck stock, and job site materials. This gives you a real-time view of where your capital is tied up without waiting for a physical count.

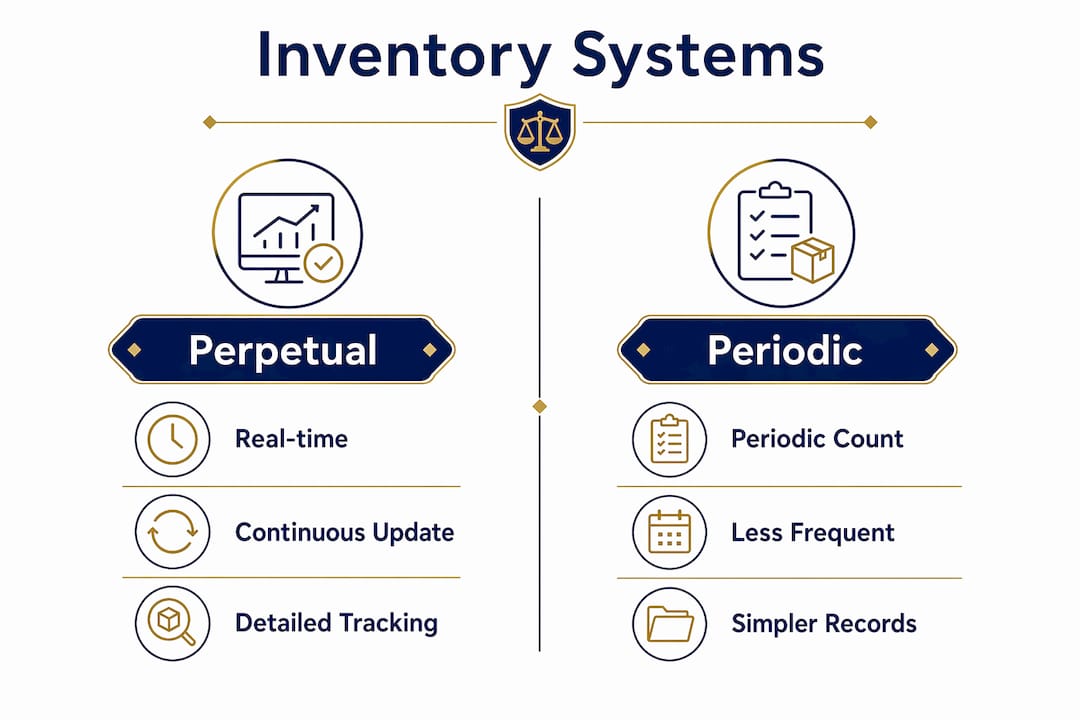

Perpetual vs. periodic: which inventory system fits HVAC?

The accounting system you choose determines how often your financial records reflect reality. For HVAC businesses, this choice has a direct impact on job costing accuracy and cash flow visibility.

Perpetual inventory systems update both the Inventory account and Cost of Goods Sold in real time with every transaction. Periodic systems update only at period-end, after a physical count is completed. The difference sounds technical, but the business impact is significant.

| Feature | Perpetual System | Periodic System |

|---|---|---|

| Inventory balance timing | Updated with every transaction | Updated at period-end only |

| COGS accuracy | Real-time, job-level | Estimated until count is done |

| Physical count requirement | Periodic verification only | Required to calculate COGS |

| Best fit for HVAC | Yes, especially multi-truck operations | Small, single-location shops only |

| Software dependency | High (ServiceTitan, QuickBooks) | Low |

| Gross margin visibility | Immediate | Delayed |

Perpetual systems are the clear choice for most HVAC businesses operating more than one truck. You cannot wait until month-end to know whether a job was profitable. If a technician completes a $4,200 repair and you do not know the parts cost until three weeks later, you cannot price the next similar job correctly.

Periodic systems work for very small shops with minimal inventory and a single location. The tradeoff is reconciliation effort. Every period-end requires a physical count, and any discrepancy between the count and your records must be investigated and adjusted. That process eats time and often reveals shrinkage, theft, or miscounting that has been building for months.

Perpetual systems are favored for real-time visibility in dynamic HVAC operations. Tools like QuickBooks integrated with field service platforms make perpetual tracking practical even for small HVAC companies. If you want to understand how QuickBooks fits your HVAC operation, the accounting setup matters as much as the software itself.

Pro Tip: Even with a perpetual system, run a physical inventory count at least twice a year. Perpetual records drift over time due to data entry errors, damaged parts, and returns that never get logged. A count catches those gaps before they distort your financial statements.

How do inventory valuation methods affect HVAC financial reporting?

Inventory valuation is the process of assigning a dollar value to the parts and materials you hold. The method you choose affects your reported Cost of Goods Sold, your ending inventory balance, your taxable income, and your gross margin. These are not small differences.

The three core methods

The three methods used in HVAC accounting are FIFO, LIFO, and weighted average cost.

- FIFO (First In, First Out): The oldest inventory costs flow through to COGS first. In an inflationary environment, FIFO produces higher ending inventory values and higher reported gross profit. This looks good on paper but increases your tax liability.

- LIFO (Last In, First Out): The most recent costs hit COGS first. LIFO reduces taxable income during periods of rising prices because higher recent costs reduce reported profit. The tradeoff is that your balance sheet carries older, lower inventory values that may not reflect replacement cost.

- Weighted Average Cost: All units are valued at the average cost of all purchases during the period. This method smooths out price fluctuations and is straightforward to apply in QuickBooks.

Inventory valuation methods like FIFO, LIFO, and weighted average significantly affect reported COGS and ending inventory values, directly impacting taxable income and net earnings. For an HVAC company buying compressors, refrigerant, and copper fittings at prices that shift with supply chains, the method you choose can mean thousands of dollars in tax differences annually.

The lower of cost or NRV rule

Under US GAAP, specifically ASC 330, inventory must be measured at the lower of cost or net realizable value. Net realizable value is the estimated selling price of the item minus any costs to complete and sell it. If the market value of a part drops below what you paid for it, you must write it down immediately. That write-down is permanent. Inventory write-downs under ASC 330 establish a non-reversible carrying value, which means you cannot reverse the write-down if prices recover later.

For HVAC businesses, this rule matters most for slow-moving or obsolete parts. An R-22 refrigerant cylinder sitting in your warehouse after the phase-out has a market value far below what you paid. Carrying it at original cost overstates your assets and your profit. Identifying and writing down obsolete inventory is not just a compliance task. It is a margin protection decision.

GAAP provides principles but not detailed rules for inventory scope and impairment, which means HVAC businesses must apply consistent judgment about obsolescence and net realizable value. That judgment needs to be documented and applied the same way every period.

How does inventory management connect to job costing and profitability?

Job costing is where inventory accounting pays off directly for HVAC businesses. Every part pulled for a job is a cost that must be assigned to that job. When that assignment happens accurately and in real time, you know your true gross margin on every ticket.

Here is the workflow that makes it work:

- Create a purchase order before ordering parts. The PO establishes the expected cost and links the purchase to a specific job or stock replenishment need.

- Match the supplier invoice to the PO upon receipt. Matching supplier invoices to POs and delivery details determines what costs capitalize to inventory versus what expenses immediately. Mismatches distort both your inventory balance and your job costs.

- Record the parts pull when the technician uses the item. This transaction moves the cost from the Inventory account to the job’s WIP or directly to COGS if the job is complete.

- Close the job and recognize revenue. At this point, all costs tied to the job, including parts, labor, and subcontractor fees, should be finalized and matched against the invoice to the customer.

- Review job-level gross margin before closing the period. Compare estimated costs to actual costs on every job above a threshold dollar amount.

Without standardized parts-to-job transactions, inventory balances may appear correct on paper but job-level costs and margins become unreliable. This is one of the most common profit leaks in HVAC businesses. The books look fine at the company level, but no one knows which jobs, service types, or technicians are actually profitable.

Supplier invoice details beyond line costs, including freight, taxes, rebates, and PO references, directly influence inventory capitalization. A $200 freight charge on a parts delivery is a real cost. If it never gets allocated to the job, your margin on that job is overstated by exactly that amount.

Pro Tip: Use equipment inventory software like MPulse or a field service platform integrated with QuickBooks to automate the parts-to-job posting. Manual entry is the single biggest source of inventory accounting errors in HVAC operations.

Inventory management becomes true accounting management when systems track status changes and integrate those changes into invoicing and replenishment workflows. That integration is the difference between knowing your numbers and guessing at them.

Key takeaways

Accurate HVAC inventory accounting requires real-time tracking, consistent valuation methods, and direct integration between parts usage and job-level cost records.

| Point | Details |

|---|---|

| Define inventory accounting clearly | HVAC inventory management is both an operational and accounting discipline requiring integrated systems. |

| Choose perpetual over periodic | Perpetual systems give real-time job cost visibility that periodic systems cannot match for multi-truck operations. |

| Apply valuation methods consistently | FIFO, LIFO, and weighted average each affect COGS and taxes differently; pick one and apply it every period. |

| Write down obsolete inventory promptly | ASC 330 write-downs are permanent, so early identification of slow-moving parts protects your margins. |

| Link every parts pull to a job | Standardized parts-to-job transactions are the foundation of accurate gross margin reporting by job and technician. |

Why most HVAC owners are flying blind on inventory costs

I have worked with enough HVAC businesses to say this plainly: the gap between field operations and accounting records is where most of the profit disappears. Technicians pull parts from trucks without logging them. Supplier invoices get paid without matching to a PO. Obsolete refrigerant sits on a shelf at original cost for two years. None of it shows up as a problem until you look at your gross margin and wonder why it is lower than your pricing should produce.

The discipline that fixes this is not complicated. It is consistent. Every parts movement needs a corresponding accounting entry. Every supplier invoice needs a PO to match against. Every job needs a cost review before you close it. When those three habits are in place, your financial reports stop being historical summaries and start being management tools.

What I see most often is owners investing in field service software like ServiceTitan but not connecting it properly to QuickBooks. The operational data exists. The accounting data exists. They just do not talk to each other. That disconnect costs real money, and it is entirely fixable with the right setup and process discipline.

The businesses that get this right treat inventory management as a financial function, not just a logistics function. They know their gross margin by job type, by technician, and by service line. They catch obsolete parts before they become write-downs. They price their work based on actual cost data, not estimates. That is the level of clarity that turns a busy HVAC company into a profitable one.

— Tony

How Truemeasureaccounting helps HVAC businesses get inventory right

If your inventory records and job costs do not match what you expect to see on your financial statements, you are not alone. Most HVAC businesses reach a point where the books need more than basic data entry.

Truemeasureaccounting specializes in HVAC bookkeeping and job costing for owner-operated businesses generating between $250,000 and $5 million annually. We connect your field operations to your accounting records, set up proper inventory tracking in QuickBooks, and give you the job-level margin data you need to make better pricing and operational decisions. Our small business bookkeeping services are available at fixed monthly pricing, so you know exactly what you are paying without hourly surprises. Schedule a free consultation to see how we can bring clarity to your HVAC financials.

FAQ

What is HVAC inventory management in accounting?

HVAC inventory management in accounting is the practice of tracking parts and materials through your accounting system, assigning costs to jobs, and valuing inventory under US GAAP standards like ASC 330 to produce accurate financial statements.

What is the difference between perpetual and periodic inventory for HVAC?

A perpetual system updates inventory and COGS in real time with every transaction, while a periodic system updates only after a physical count at period-end. Perpetual systems are better for HVAC businesses that need job-level cost visibility.

Which inventory valuation method is best for HVAC businesses?

FIFO, LIFO, and weighted average are all acceptable under US GAAP. LIFO reduces taxable income during inflation, while FIFO produces higher reported profit. The best method depends on your tax strategy and how consistently you can apply it.

Why does inventory accuracy affect HVAC job profitability?

When parts costs are not properly assigned to jobs, your gross margin data becomes unreliable. You may appear profitable at the company level while losing money on specific job types, technicians, or service lines.

What software supports HVAC inventory accounting?

ServiceTitan integrates field inventory tracking with accounting workflows, while QuickBooks handles the financial recording side. Connecting the two with proper setup is what produces accurate, real-time job costing data.