Setting up accounting as a real estate investor means building a property-specific financial system that tracks income and expenses by unit, maximizes deductions, and keeps you tax-ready year-round. The industry term for this practice is real estate investor bookkeeping, and it goes well beyond basic spreadsheets or generic small business accounting. Investors who get this right spend less time scrambling at tax time, catch cash flow problems early, and make better decisions about which properties to keep, sell, or refinance. This guide walks you through every layer of that system, from entity setup to software selection to weekly routines that take less time than a lunch break.

How to set up accounting as a real estate investor: what you need first

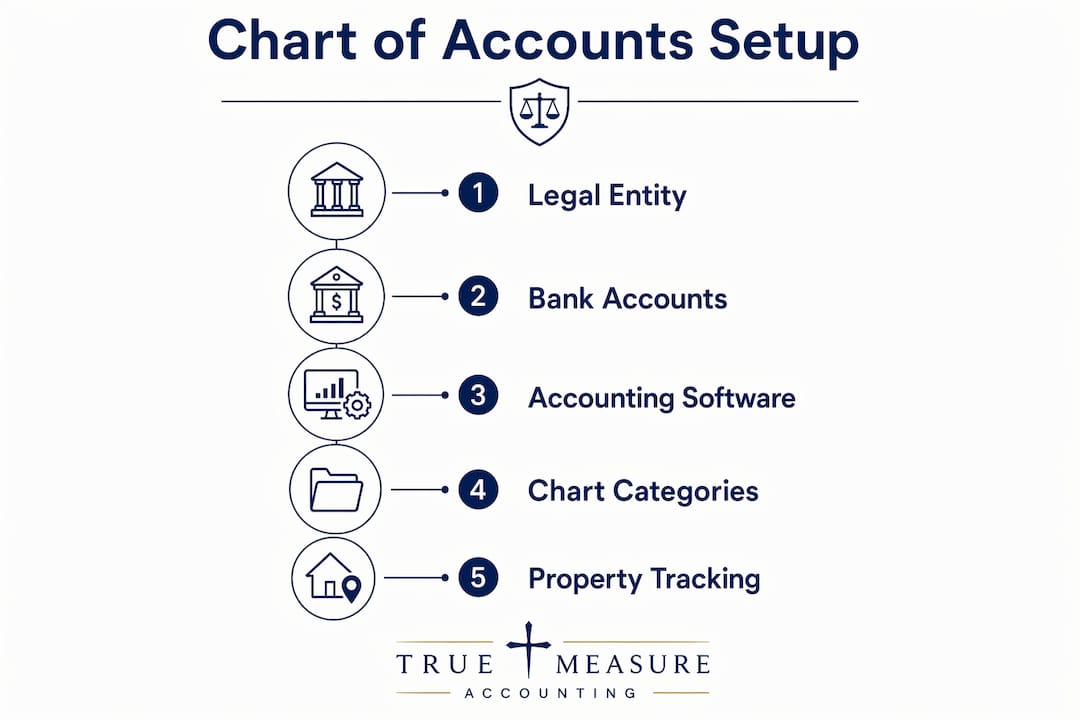

Before you open any software or create a single account, you need the right foundation. The structure you choose now determines how clean your books stay as your portfolio grows.

Choose your legal entity first. Most investors operate as a sole proprietor or through a single-member LLC. Each choice carries different tax and liability implications. An LLC gives you liability protection and the option to elect S-corp taxation later. A sole proprietor files everything on Schedule E of their personal return. Either way, your accounting system must match your entity structure from day one.

Open dedicated bank accounts. Separate operating accounts and security deposit trust accounts are not optional. Commingling personal and rental funds is the single fastest way to lose deductions during an audit. Open at minimum three accounts: one for operating income and expenses, one for security deposits, and one for reserves or capital improvements. This structure makes reconciliation clean and protects you legally.

Select your accounting software before you record a single transaction. Generic tools like QuickBooks Online work well if you configure them correctly for real estate. Specialized platforms like Baselane and Stessa are built specifically for landlords and require less setup. Your choice here shapes everything downstream, including how you generate Schedule E reports and how you track performance by property.

Prepare a rental-specific chart of accounts. A chart of accounts is the master list of every category you will use to record transactions. A real estate chart of accounts must align with Schedule E line items so your books translate directly to your tax return. Without this alignment, your bookkeeper or CPA spends extra hours reclassifying transactions every year.

Here is what you need before going live:

- A registered legal entity (LLC or sole proprietor) with an EIN from the IRS

- A dedicated business checking account for rental operations

- A separate trust account for tenant security deposits

- A reserve account for repairs and capital expenditures

- Accounting software configured for real estate

- A Schedule E-aligned chart of accounts

| Prerequisite | Why it matters |

|---|---|

| Dedicated operating account | Prevents commingling and simplifies reconciliation |

| Security deposit trust account | Required by law in most states; keeps deposits legally separate |

| Reserve account | Tracks capital spending separately from operating expenses |

| Legal entity (LLC or sole proprietor) | Determines tax filing method and liability exposure |

| Real estate chart of accounts | Aligns bookkeeping with Schedule E for accurate tax reporting |

How to create a Schedule E-mapped chart of accounts for property investors

A chart of accounts is the backbone of your entire accounting system for property investors. Every transaction you record flows into one of these categories, so getting the structure right from the start saves hundreds of hours over the life of your portfolio.

The standard structure uses block numbering to organize account types. Block numbering assigns number ranges to each category: 1000s for assets, 2000s for liabilities, 3000s for equity, 4000s for revenue, and 5000s for expenses. This system scales cleanly as you add properties, entities, or investors without rebuilding your books.

The five core account categories for rental investors

Assets (1000s) include your bank accounts, security deposit funds held, accounts receivable for unpaid rent, and the value of your properties. Each property should have its own asset account for the building and a separate one for land, since land is not depreciable.

Liabilities (2000s) cover mortgage balances, security deposits held as liabilities, and any accounts payable. Tracking your mortgage balance here gives you an accurate net worth picture at any point in time.

Equity (3000s) reflects your ownership stake after liabilities. For investors with multiple properties or partners, equity accounts track each owner’s contribution and distribution history.

Revenue (4000s) is where rental income, late fees, pet fees, and parking income all live. Each income type gets its own account so you can see exactly what is driving revenue across your portfolio.

Expenses (5000s) map directly to Schedule E line items: advertising, auto and travel, cleaning and maintenance, insurance, legal and professional fees, management fees, mortgage interest, repairs, supplies, taxes, utilities, and depreciation. Every expense category on Schedule E should have a matching account in your books.

Tracking by property with classes or sub-accounts

The most powerful feature of a well-built chart of accounts is property-level tracking. QuickBooks Online uses a “class” feature to tag every transaction to a specific property. Baselane and Stessa do this natively at the property level. This means you can pull a profit and loss statement for a single address in seconds, which is exactly what you need to decide whether a property is worth keeping.

Pro Tip: Create a sub-account or class for each property at setup, even if you only own one. Adding the structure now costs nothing. Retrofitting it after 200 transactions is expensive and error-prone.

Here is a sample expense account structure aligned to Schedule E:

- 5100 Advertising

- 5200 Auto and travel

- 5300 Cleaning and maintenance

- 5400 Insurance

- 5500 Legal and professional fees

- 5600 Management fees

- 5700 Mortgage interest

- 5800 Repairs

- 5900 Supplies

- 6000 Property taxes

- 6100 Utilities

- 6200 Depreciation expense

| Generic account name | Schedule E line item | Notes |

|---|---|---|

| Repairs | Repairs | Separate from capital improvements |

| Management fees | Management fees | Track per property |

| Mortgage interest | Mortgage interest paid | Matches Form 1098 |

| Insurance | Insurance | Includes landlord and umbrella policies |

| Depreciation | Depreciation | Calculated separately; entered as journal entry |

What does a weekly 15-minute bookkeeping routine look like?

A professional-grade bookkeeping system for rental properties requires only 15 minutes per week when you build the right habits from the start. That consistency turns bookkeeping from a year-end tax scramble into a real-time view of your portfolio’s health.

Here is the exact weekly routine that works:

-

Log in and import transactions. Most software connects directly to your bank accounts and pulls in new transactions automatically. Baselane and Stessa both offer bank feeds that categorize common transactions on import.

-

Review and confirm categorizations. Automated categorization is accurate for recurring items like mortgage payments and utility bills. Spend two minutes reviewing any uncategorized or miscategorized transactions and correct them immediately.

-

Attach receipts to expense transactions. Automated receipt attachment via mobile apps is the fastest way to build audit-ready records. Take a photo of any paper receipt and attach it to the matching transaction before you forget what it was for.

-

Review rent receivables. Check which tenants have paid and which have not. Running aged receivables reports weekly lets you send late notices before small delays become serious collection problems.

-

Record any cash or check payments manually. Cash transactions do not appear in bank feeds. Log them manually with a note describing the payment and the property it relates to.

-

Update your security deposit ledger. Every deposit received, applied, or returned needs a matching entry. Security deposit accounting is heavily regulated in most states, and errors here create legal exposure.

-

Run a quick profit and loss by property. A 30-second glance at each property’s monthly numbers tells you whether income and expenses are tracking as expected. Flag anything unusual for follow-up.

Pro Tip: Schedule your 15-minute bookkeeping session at the same time every week, such as monday morning before you check email. Consistency is what makes the system work. Missing two weeks in a row is where backlogs start.

The biggest mistake investors make is skipping weeks and then trying to catch up in bulk. Bulk catch-up work is slow, error-prone, and strips away the early-warning benefit that weekly bookkeeping provides. Good bookkeeping habits directly improve profitability because you spot problems while they are still small.

Which accounting software fits your real estate portfolio?

Generic accounting software lacks native support for real estate nuances like depreciation schedules, cost segregation, and multi-entity portfolios. This is not a minor gap. Investors who use general-purpose tools without customizing them end up with books that do not match their tax returns and reports that do not answer the questions they actually need answered.

The right investor accounting software depends on your portfolio size and complexity.

Stessa is the best starting point for residential landlords with smaller portfolios. Stessa offers a free-to-start platform designed for up to 25 properties, with automated transaction import and tax-ready reports. It is limited for commercial properties or multi-entity structures, but for a landlord with 1–10 units, it removes most of the manual work.

Baselane sits in the middle of the market. It combines banking, rent collection, and bookkeeping in one platform. The chart of accounts is pre-built for real estate, and the property-level reporting is strong. Investors managing 5–30 units who want an all-in-one tool find it well-suited to their needs.

Agora serves larger and more complex portfolios. Agora provides accounting features including K-1 delivery, investor distributions, and multi-entity management. It fits syndicators, fund managers, and investors with commercial assets who need institutional-grade reporting.

QuickBooks Online remains a strong option when configured correctly. It requires more setup than the real estate-specific tools, but it integrates with more third-party services and gives you access to a larger pool of bookkeepers and CPAs who know the platform.

| Platform | Best for | Key strength | Limitation |

|---|---|---|---|

| Stessa | 1–25 residential units | Free, automated, tax-ready | No multi-entity or commercial support |

| Baselane | 5–30 units, all-in-one | Banking + bookkeeping combined | Less flexible for complex structures |

| Agora | Syndicators, large portfolios | K-1 delivery, multi-entity | Higher cost, steeper learning curve |

| QuickBooks Online | Any size with proper setup | Broad integrations, wide CPA support | Requires real estate-specific configuration |

Key features to require from any platform you choose:

- Property-level profit and loss reporting

- Bank feed integration for automated transaction import

- Schedule E-aligned expense categories

- Depreciation tracking or journal entry support

- Audit-ready document storage

How do property-level financial reports improve your investment decisions?

Consistent property-level profit and loss reviews help investors identify underperforming assets and optimize portfolio returns before tax season. A report you only look at in april is a report that cannot help you make decisions in july.

The three reports every investor needs are the profit and loss by property, the cash flow statement, and the balance sheet. Each one answers a different question.

The profit and loss by property shows whether a specific address is making or losing money after all operating expenses. If one property consistently shows thin margins, you can investigate whether the issue is vacancy, high maintenance costs, or below-market rents before the problem compounds.

The cash flow statement shows actual cash moving in and out, separate from accounting entries like depreciation. A property can show a paper loss due to depreciation while generating strong positive cash flow. Understanding this distinction is critical for refinancing decisions and for evaluating whether to hold or sell.

The balance sheet shows what you own, what you owe, and what your net equity position is across the portfolio. Lenders look at this report when you apply for new financing. Keeping it accurate and current gives you a real-time picture of your borrowing capacity.

Here is what to look for in each monthly review:

- Gross rental income versus expected rent roll (flag vacancies immediately)

- Repair and maintenance costs as a percentage of property value (above 1.5% annually warrants attention)

- Mortgage interest versus principal paydown (tracks equity building over time)

- Net operating income by property (the core profitability metric for each asset)

- Any expense categories trending higher than the prior three months

Professional financial reporting gives you these reports in a format that is ready to share with lenders, partners, or a CPA. When your books are clean and your reports are current, tax preparation becomes a straightforward process rather than a reconstruction project.

Key takeaways

A well-built accounting system for property investors is the difference between managing your portfolio and being managed by it.

| Point | Details |

|---|---|

| Build the foundation first | Open dedicated operating, security deposit, and reserve accounts before recording any transactions. |

| Use a Schedule E-mapped chart of accounts | Align every expense category to Schedule E line items to make tax preparation direct and accurate. |

| Keep a weekly 15-minute routine | Consistent weekly bookkeeping prevents backlogs and gives you real-time cash flow visibility. |

| Match software to portfolio complexity | Stessa fits small residential portfolios; Baselane suits mid-size; Agora handles multi-entity and syndications. |

| Review property-level reports monthly | Profit and loss by property identifies underperformers before they drag down your overall returns. |

What I have learned from setting up real estate accounting the right way

The investors I work with who struggle most with their books share one common trait: they treated accounting as a year-end task instead of a weekly operating habit. By the time they came to us, they had 18 months of uncategorized transactions, no idea which properties were actually profitable, and a tax bill that surprised them. That is not a software problem. That is a discipline problem.

The fix is simpler than most people expect. A 15-minute weekly session, the right chart of accounts, and a platform that matches your portfolio size will handle 90% of the work. The remaining 10% is knowing what the reports are telling you and acting on that information.

One thing I see investors get wrong consistently is choosing software based on price alone. Stessa is free, and that is genuinely useful for a first-time landlord with two units. But when you have five properties across two LLCs and a partner who needs quarterly distributions, free software creates more problems than it solves. The cost of the right tool is almost always less than the cost of cleaning up the wrong one.

The other mistake is skipping the entity and banking structure step. I have seen investors with 10 properties running everything through a personal checking account. Their books are a legal and tax liability waiting to happen. Separating accounts is not bureaucracy. It is the foundation that makes everything else work.

My honest advice: get the structure right in the first 30 days, build the weekly habit, and let the software do the heavy lifting. If your portfolio grows past 10 units or you add a second entity, bring in a professional to review your setup. A few hours of expert review at that stage saves you from a full cleanup later.

— Tony

Truemeasureaccounting works with real estate investors every day

Real estate investors need more than a bookkeeper who enters data. They need someone who understands property-level performance, Schedule E reporting, and how clean books connect to better investment decisions.

Truemeasureaccounting provides rental property bookkeeping services built specifically for investors managing single-family homes, multi-family units, and mixed portfolios. We set up your chart of accounts, maintain your weekly reconciliations, and deliver property-level reports you can actually use. Our fixed-price bookkeeping model means no surprise invoices at year-end. If you are ready to stop guessing at your numbers and start making decisions based on real data, schedule a free consultation at truemeasureaccounting.com.

FAQ

What accounts do I need to set up accounting as a real estate investor?

You need at minimum a dedicated operating checking account, a security deposit trust account, and a reserve account for capital expenses. Keeping these separate from personal finances is the foundation of clean real estate investor bookkeeping.

What is a Schedule E chart of accounts?

A Schedule E chart of accounts is a list of income and expense categories that maps directly to IRS Schedule E, the form used to report rental income and losses. Aligning your books to Schedule E makes tax preparation accurate and reduces CPA reclassification work.

How often should I do bookkeeping for rental properties?

Weekly bookkeeping is the standard for rental property investors. A 15-minute weekly session covers bank reconciliation, transaction categorization, receipt attachment, and rent receivable review.

What is the best accounting software for real estate investors?

The best choice depends on portfolio size. Stessa works well for residential landlords with up to 25 properties. Baselane suits investors who want banking and bookkeeping combined. Agora fits larger portfolios with multi-entity structures and investor distributions.

When should I hire a professional accountant for my rental properties?

Hire a professional when you add a second entity, take on a partner, or own more than five properties. A professional review at that stage catches structural problems early and sets up your accounting system for property investors to scale without costly corrections.