Year-end tax strategy is the deliberate planning and execution of financial decisions before december 31 to reduce your tax liability and improve your business’s financial position. For service business owners, whether you run an HVAC company, a plumbing operation, a general contracting firm, or a professional services practice, understanding how year-end tax strategy works for your business is the difference between writing a large check to the IRS and keeping that money working in your company. The core moves involve timing income and deductions, making retirement contributions, placing capital assets in service, and managing estimated tax payments. None of this is complicated when you know the rules. All of it requires action before the calendar flips.

What are the key components of an effective year-end tax strategy?

Year-end tax planning is built around five core levers. Each one reduces your taxable income in a different way, and the best results come from using several of them together.

Retirement plan contributions are one of the most powerful tools available to service business owners. A Solo 401(k) or SEP IRA lets you move significant income out of your taxable column and into a tax-deferred account. The SECURE 2.0 Act changed the rules in your favor: Solo 401(k) contributions can now be made retroactively in the plan’s first year, covering both employer and employee amounts up to the tax filing deadline including extensions.

Capital asset purchases under Section 179 and bonus depreciation let you deduct the full cost of qualifying equipment in the year you buy it, rather than spreading it over years. An HVAC company buying a new service van, or an electrical contractor purchasing diagnostic equipment, can write off the full purchase price in the current tax year. The asset must be placed in service by december 31 to qualify.

Income and expense timing is about controlling when money hits your books. Cash-basis businesses can accelerate deductions by paying bills before year-end and defer income by delaying invoices until january. Accrual-basis businesses follow different rules, but the principle of timing still applies.

Here are the five levers in summary:

- Retirement contributions: Solo 401(k) or SEP IRA contributions reduce taxable income dollar for dollar.

- Asset depreciation: Section 179 and bonus depreciation allow full-year deductions on qualifying purchases placed in service by december 31.

- Expense acceleration: Prepay legitimate business expenses before year-end to pull deductions into the current tax year.

- Income deferral: Delay billing or receipt of income until january when your tax bracket allows it.

- Estimated tax payments: Make your Q4 payment by january 15 to avoid IRS underpayment penalties.

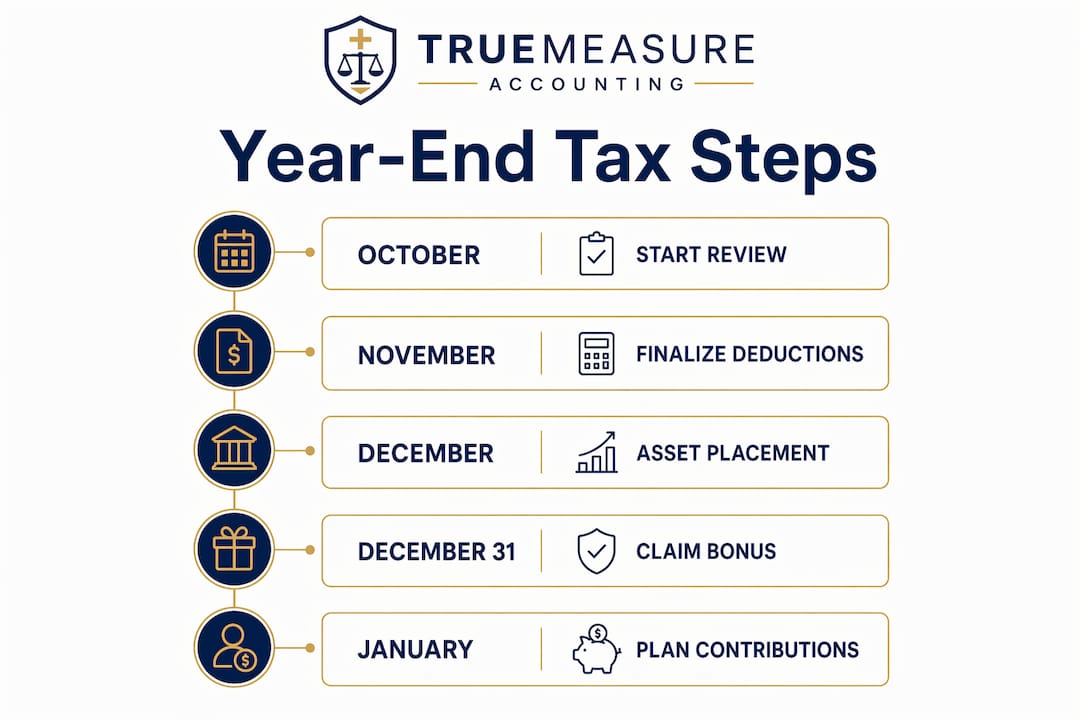

Pro Tip: Review your profit and loss statement in october, not december. You need at least 60 days to execute most of these moves before the deadline.

How do business structure and income projection shape your tax decisions?

Business structure influences not only what taxes you owe but also how payments and deductions work. A sole proprietor, an S-corporation owner, and a C-corporation owner each face different tax mechanics at year-end. Getting this wrong means applying the right strategy to the wrong entity type, which can cost you deductions or create unexpected tax bills.

Your projected taxable income determines which strategies deliver the most value. A contractor expecting $180,000 in net income benefits differently from a retirement contribution than one expecting $80,000. Year-end strategies are most effective when matched precisely to projected taxable income because the tax benefit varies by bracket and eligibility.

Building a pro forma tax return early in Q4 gives you a clear baseline. Your tax advisor runs your numbers as if the year ended today, then identifies the gap between your current liability and your target. That gap tells you exactly how much to put into retirement accounts, what equipment to buy, and whether deferring income makes sense.

Key questions your income projection should answer:

- What is your estimated net taxable income before any year-end moves?

- Which tax bracket does that income land in, and what is the marginal rate?

- Do you face self-employment tax, and how do retirement contributions reduce that exposure?

- Are you at risk of an IRS underpayment penalty based on your Q1 through Q3 estimated payments?

The IRS recommends paying taxes as income is earned through withholding or estimates. Q4 estimated payments are generally due by january 15 of the following year. Missing that date adds penalties on top of your tax bill.

What timing and documentation requirements apply to year-end tax moves?

Timing is where most business owners lose deductions they thought they had locked in. The IRS does not care that you ordered the equipment in november. It cares whether the asset was available and in use by december 31.

Here is the correct sequence for executing the most common year-end moves:

- Run your income projection in october. You need real numbers to make real decisions. Guessing your income bracket leads to over-contributing or under-contributing to retirement accounts.

- Purchase and place capital assets in service before december 31. Proof of placed-in-service status includes procurement schedules, operational confirmation, and physical work tests. A purchase invoice alone is not enough.

- Pay or accrue all accelerated expenses by december 31. Expense acceleration deductions require supporting documentation proving ordinary business necessity and payment or accrual by year-end. Ordering supplies and receiving an invoice is not the same as paying for them.

- Adopt your retirement plan before the deadline. Solo 401(k) plans have specific adoption deadlines. Under SECURE 2.0, retroactive contributions are allowed in the plan’s first year up to the tax filing deadline including extensions, but the plan itself must be properly established.

- Make your Q4 estimated tax payment. Submit by january 15 to avoid penalties. If you have had a strong year, this payment may be larger than your previous quarters.

Pro Tip: Keep a year-end tax file with four folders: asset purchase records, retirement plan documents, expense receipts paid before december 31, and your Q4 estimated payment confirmation. If you get audited, this file is your defense.

The table below shows the critical deadlines for the most common year-end tax moves:

| Tax Move | Deadline | Documentation Required |

|---|---|---|

| Section 179 / bonus depreciation | December 31 | Proof of placed-in-service, operational records |

| Cash-basis expense acceleration | December 31 | Receipts showing payment before year-end |

| Solo 401(k) plan adoption | October 15 (following year, first year only) | Plan documents, adoption agreement |

| Solo 401(k) contributions | Tax filing deadline including extensions | Contribution records, plan statements |

| Q4 estimated tax payment | January 15 | IRS payment confirmation |

| Charitable contributions | December 31 | Acknowledgment letter from recipient organization |

How can year-end tax moves improve your cash flow and profitability?

Tax savings are not just about paying less to the IRS. They directly affect your cash position and your ability to reinvest in the business. A plumbing company that saves $15,000 in taxes through a combination of retirement contributions and equipment depreciation has $15,000 more to put toward a new crew, better tools, or a marketing push in Q1.

The connection between tax strategy and cash flow works in both directions. Prepaying expenses before year-end reduces your cash balance temporarily but creates a deduction that lowers your tax bill in april. That trade-off is worth calculating before you act, not after.

Here is how each major lever affects your cash flow:

- Retirement contributions move cash out of your operating account and into a tax-deferred account. You lose liquidity short-term but gain it back through a lower tax bill and long-term wealth building.

- Equipment purchases require upfront cash or financing, but the full depreciation deduction in year one means the government effectively subsidizes part of the purchase price.

- Expense prepayment accelerates cash outflows but pulls deductions forward. This works best when you have strong cash reserves and expect a higher tax rate this year than next.

- Income deferral keeps cash out of your account until january, which can feel uncomfortable but reduces your current-year tax exposure.

- Estimated tax payments spread your tax liability across the year. Paying consistently through Q1 to Q4 prevents a large cash drain in april and avoids IRS penalties.

The year-end tax planning checklist from Truemeasureaccounting walks service business owners through each of these moves with specific timing guidance. Managing these decisions well is how you turn tax planning into a cash flow tool, not just a compliance exercise.

What 2026 tax law changes affect service business owners?

Several 2026 updates change the math on common year-end strategies. Service business owners need to know these before executing their plans.

| Tax Area | Pre-2026 Rule | 2026 Change |

|---|---|---|

| Bonus depreciation | Phasing down from 100% | IRS Notice 2026-11 confirms updated placed-in-service guidance for 100% bonus depreciation |

| Charitable deductions | Deductible above standard threshold | Starting 2026, itemizers can only deduct charitable gifts above 0.5% of AGI |

| Solo 401(k) contributions | Employee deferrals required by Dec 31 | SECURE 2.0 allows retroactive deferrals in the plan’s first year up to the filing deadline |

| Estimated tax timing | Q4 due january 15 | No change; IRS enforcement of underpayment penalties remains active |

The charitable contribution change is significant for business owners who use bunching strategies or donor-advised funds. The 0.5% of adjusted gross income floor means smaller contributions may no longer generate an itemized deduction. If charitable giving is part of your tax plan, the timing and amount need to be recalculated for 2026.

The SECURE 2.0 retirement contribution flexibility is a genuine advantage. If you have not yet adopted a Solo 401(k) and you are self-employed or running an owner-operated service business, you now have more time to act. The key is getting the plan documents in place correctly, not just making a contribution and hoping it qualifies.

October and november are critical months for finalizing year-end deductions because many moves cannot be done retroactively after year-end. The 2026 updates make early planning even more important, since some rules now require additional documentation or have new eligibility thresholds.

Key Takeaways

Effective year-end tax strategy for service businesses requires matching the right moves to your projected income, executing transactions before december 31, and keeping documentation that proves each deduction is legitimate.

| Point | Details |

|---|---|

| Start planning in october | Most year-end tax moves require real transactions that cannot be executed after december 31. |

| Match strategy to income projection | Build a pro forma tax return to identify your bracket and target the highest-value deductions first. |

| Document asset placement carefully | Proof of placed-in-service status requires operational records, not just a purchase invoice. |

| Use SECURE 2.0 retirement flexibility | Solo 401(k) contributions can be made retroactively in the plan’s first year up to the filing deadline. |

| Treat tax savings as a cash flow tool | Every dollar saved in taxes is a dollar available for reinvestment, payroll, or business growth. |

What I have learned from 20 years of running service businesses

Running multi-million-dollar service operations taught me something most tax articles skip: the business owners who pay the least in taxes are not the ones with the most aggressive strategies. They are the ones with the most organized books.

You cannot execute a year-end tax plan if you do not know your actual net income in october. Most service business owners I have worked with find out their real numbers in february, when their accountant is preparing their return. By then, every deadline has passed. The retirement contribution window is closed. The equipment that could have been placed in service is sitting in a warehouse with no documentation. The Q4 estimated payment was missed or underpaid.

The fix is not a more complex tax strategy. The fix is clean, current financials. When your books are up to date through september, you can run a real income projection, identify the right moves, and execute them with six to ten weeks to spare. That is when tax planning actually works.

I also want to push back on the idea that year-end tax planning is a one-time event. The best tax outcomes come from decisions made throughout the year. Pricing your jobs correctly, managing your payroll structure, tracking every deductible expense in real time, and reviewing your financials monthly. Year-end is when you finalize and execute. The groundwork should already be laid.

If you are a contractor, an HVAC owner, or a plumber reading this in november and realizing your books are a mess, the first step is not to call a tax attorney. The first step is to get your financials current. Everything else follows from that. You can review tax strategies for service firms to see how clean books translate directly into lower tax bills.

— Tony

How Truemeasureaccounting supports your year-end tax planning

Truemeasureaccounting works with owner-operated service businesses across the country to build the financial clarity that makes year-end tax planning actually work. That means current books, accurate income projections, and a clear picture of which moves will have the biggest impact on your tax bill before december 31.

If your books are behind, your Q4 numbers are unclear, or you are not sure which deductions you qualify for, Truemeasureaccounting can help you get organized and execute before the deadline. The firm’s small business tax services cover everything from bookkeeping cleanup to proactive tax strategy built around your specific business structure and income. You can also explore the firm’s bookkeeping services to see how accurate monthly financials become the foundation for every tax decision you make.

FAQ

What is year-end tax strategy for a business?

Year-end tax strategy is the process of timing income, deductions, asset purchases, and retirement contributions before december 31 to legally reduce your taxable income and lower your tax bill.

When should a service business owner start year-end tax planning?

October is the right time to start. Most year-end tax moves require real transactions that must be completed before december 31, and many cannot be done last minute.

What is the deadline for placing assets in service for bonus depreciation?

Assets must be placed in service by december 31 of the tax year. A purchase invoice is not sufficient. You need operational records proving the asset was available and in use by year-end.

Can I still set up a Solo 401(k) after december 31?

Under SECURE 2.0, a Solo 401(k) adopted in the plan’s first year allows retroactive contributions up to the tax filing deadline including extensions, but the plan must be properly established with correct documentation.

How does year-end tax planning affect cash flow?

Tax savings reduce the cash you send to the IRS, which keeps more money in your business. Strategic moves like retirement contributions and equipment depreciation lower your tax bill while building long-term assets, making them a direct cash flow benefit.