Reducing taxes for a professional service firm is a direct result of four integrated strategies: entity structuring, compensation optimization, qualified retirement plan design, and proactive credit documentation. Most firm owners rely on a single CPA filing a return once a year. That approach leaves real money on the table. The standard industry term for what you actually need is proactive tax planning, and it goes well beyond deductions. This guide covers each strategy in practical terms, with the implementation steps and real-world context you need to act on them.

How does entity structuring reduce taxes for a professional service firm?

Entity structure is the single most impactful lever for reducing your firm’s tax liability, and most owners set it once and never revisit it. The legal form your business operates under determines how income is taxed, how self-employment taxes are calculated, and whether certain income-splitting strategies are even available to you.

The four most common structures for professional service firms are sole proprietorships, LLCs, S-Corporations, and C-Corporations. Each carries a different tax profile.

| Entity Type | Self-Employment Tax Exposure | Key Tax Advantage |

|---|---|---|

| Sole Proprietorship | 100% of net profit | Simple filing; no advantage |

| Single-Member LLC | 100% of net profit | Pass-through; liability protection |

| S-Corporation | Only on reasonable salary | Distributions avoid payroll tax |

| C-Corporation | None at entity level | Flat 21% rate; fringe benefit deductions |

S-Corps are the most commonly used structure for tax reduction in professional service firms. The core benefit is that S-Corp distributions avoid the 15.3% self-employment tax that sole proprietors and single-member LLC owners pay on every dollar of profit. If your firm earns $400,000 in net income and you pay yourself a $120,000 reasonable salary, only that salary is subject to payroll taxes. The remaining $280,000 passes through as a distribution, free of self-employment tax. That is a material savings.

However, legal restructuring such as entity conversions and holding company setups requires attorney-CPA collaboration, not just an accounting decision. Many owners mistakenly rely only on standard accounting and miss the complex legal strategies that yield greater savings. A holding company structure, for example, can separate operating income from investment assets, creating additional tax planning opportunities across multiple entities.

Pro Tip: The IRS scrutinizes S-Corp owners who pay themselves an unreasonably low salary to maximize distributions. Work with both a CPA and a business attorney to set a defensible reasonable compensation figure based on industry benchmarks and your actual role in the firm.

If you work with attorneys and need specialized accounting support for that collaboration, the article on law firm accounting compliance covers why that interdisciplinary relationship matters for service firms specifically.

What compensation strategies lower taxes while keeping you compliant?

Once your entity structure is right, the next step is optimizing how you pay yourself. Owner compensation in a professional service firm is not just a payroll decision. It is a tax planning decision with significant consequences.

Here is a practical framework for thinking through compensation optimization:

-

Set a defensible reasonable salary. In an S-Corp, your salary must reflect what you would pay someone else to do your job. Underpaying yourself to avoid payroll taxes is the most common trigger for IRS audits of S-Corp owners. Use Bureau of Labor Statistics wage data or industry compensation surveys to support your number.

-

Take the remainder as distributions. Once your salary is set, excess profits can be distributed to you as an owner distribution. These are not subject to FICA taxes, which saves you up to 15.3% on every dollar distributed above your salary threshold.

-

Time bonuses and income recognition strategically. If your firm uses cash basis accounting for tax purposes, you control when income is recognized and when expenses are deducted. Delaying an invoice to January or accelerating a December expense payment can shift taxable income between years. This is especially useful when you expect your tax bracket to change.

-

Layer in qualified retirement plan contributions. Retirement plan contributions reduce your W-2 income and your firm’s taxable income simultaneously. This is covered in depth in the next section, but it belongs in your compensation planning conversation from the start.

-

Use fringe benefits to replace taxable compensation. Health insurance premiums, HSA contributions, and accountable plan reimbursements can replace taxable salary with tax-free compensation. A C-Corp structure offers the broadest access to these benefits, which is one reason some high-income firm owners consider a C-Corp despite the double-taxation concern.

The most common pitfall in compensation planning is treating it as a one-time setup rather than an annual review. Your revenue, bracket, and business structure may all change. What was optimal at $500,000 in revenue may not be optimal at $1.5 million.

Pro Tip: If your firm has multiple owners, compensation planning becomes more complex. Unequal distributions, guaranteed payments in partnerships, and varying ownership percentages all affect each owner’s tax outcome differently. Model each scenario before the tax year ends, not after.

How can qualified retirement plans dramatically reduce taxable income?

Qualified retirement plans are the most underutilized tax reduction tool available to professional service firm owners. The contribution limits far exceed what most owners realize, and the tax impact compounds over time.

Cash balance and defined benefit plans can shelter $60,000 to $300,000 or more from taxable income each year. Owners aged 50 and above can contribute $100,000 to $200,000 annually to these plans, generating a 5 to 10 times return on investment by reducing income taxed at the highest marginal rates. That is not a minor adjustment. For a firm owner in the 37% federal bracket, a $200,000 contribution produces $74,000 in immediate federal tax savings, before state taxes.

Here is how the most relevant plan types compare for professional service firm owners:

- SEP-IRA: Contributions up to 25% of compensation, capped at $69,000 in 2025. Simple to set up, no annual filing requirement. Best for solo practitioners or firms with few employees.

- Solo 401(k): Combines employee and employer contributions for a combined limit of $69,000 ($76,500 if age 50 or older). Requires no employees other than the owner and spouse.

- Cash Balance Plan: A defined benefit plan that allows contributions based on age and income. Owners in their 50s can contribute $150,000 to $300,000 annually. Requires actuarial certification and annual funding.

- Defined Benefit Plan: The highest contribution limits available. Designed for owners with consistent high income who want maximum tax sheltering. Requires long-term commitment and professional plan administration.

The implementation sequence matters. Start with a SEP-IRA or Solo 401(k) in the early years of your firm. As revenue grows and your income stabilizes above $500,000, engage a retirement plan specialist to model whether a cash balance plan layered on top of a 401(k) makes sense. The combination can shelter well over $200,000 annually for owners in their late 40s and 50s.

One important integration point: retirement plan contributions reduce your qualified business income (QBI) deduction base. Your CPA needs to model the net effect before you finalize contribution amounts each year. The gross tax savings from the contribution may be partially offset by a reduced QBI deduction, so the optimal contribution is not always the maximum contribution.

What proactive methods maximize tax credits and deductions for service firms?

Tax credits are more valuable than deductions because they reduce your tax bill dollar for dollar rather than reducing taxable income. The problem is that maximizing tax credits is hampered mainly by poor documentation rather than lack of eligibility. Most service firm owners qualify for credits they never claim because they cannot substantiate the activity at year-end.

The credits most relevant to professional service firms include:

- Research and Development (R&D) Tax Credit: Available to firms that develop or improve processes, software, or methodologies. Engineering firms, IT consultants, and architecture firms frequently qualify. The credit equals 20% of qualifying research expenses above a base amount.

- Section 179D Energy Efficiency Deduction: Available to firms that design energy-efficient commercial buildings. Architecture and engineering firms that certify qualifying projects can claim up to $5.00 per square foot.

- Work Opportunity Tax Credit (WOTC): Available when you hire employees from targeted groups including veterans and long-term unemployment recipients. The credit ranges from $1,200 to $9,600 per qualifying hire.

- State-Level Credits: Many states offer credits for job creation, investment in economically distressed areas, or industry-specific activities. These are frequently overlooked and vary significantly by state.

The fix for documentation gaps is project-based accounting with real-time activity tagging. Implementing project codes in QuickBooks, Xero, or similar platforms transforms credit substantiation from a stressful year-end scramble into an automated process. When your team logs time and expenses against tagged project codes throughout the year, the documentation exists when you need it.

Pro Tip: Set up a quarterly credit review with your CPA, not just an annual one. Credits like R&D require contemporaneous documentation. If you wait until December to reconstruct records from January, the IRS will not accept them.

The tax credit market also offers arbitrage opportunities through buying and selling transferable credits. Some states allow credits to be transferred between taxpayers, which means you may be able to purchase credits at a discount to offset your state tax liability. This requires due diligence and proper indemnification clauses, but it is a legitimate strategy for firms with significant state tax exposure.

For firms that want to see how cloud-based accounting tools support real-time credit tracking, Truemeasureaccounting’s accounting technology consulting page covers the platforms and setup approaches that make this practical.

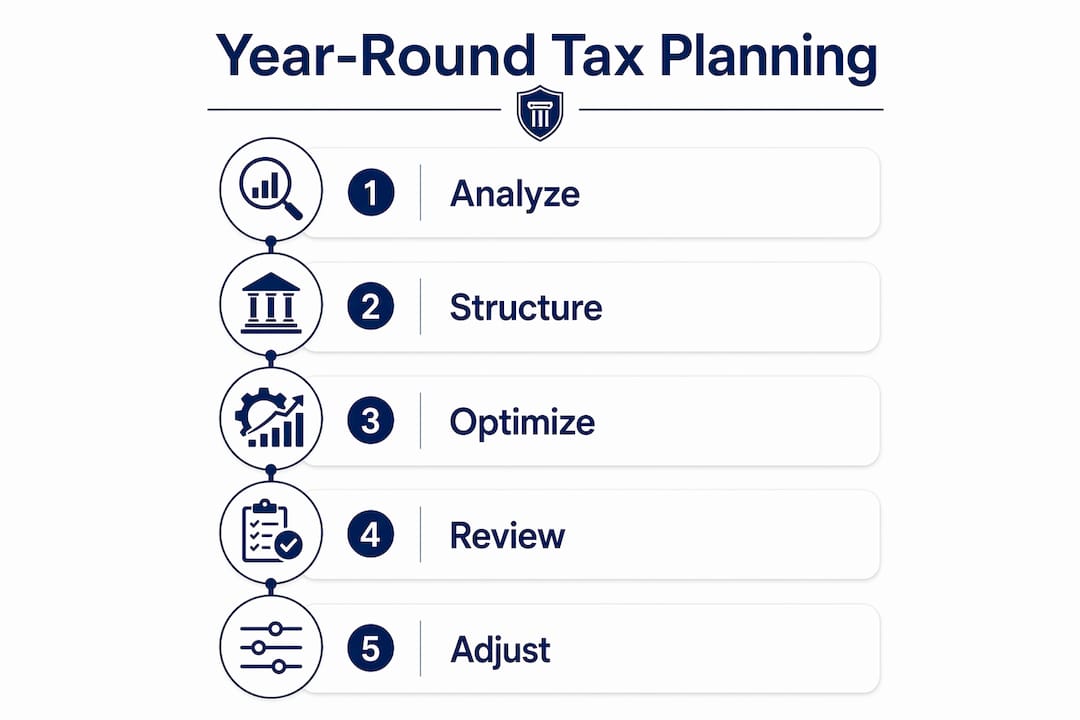

How does year-round tax planning improve outcomes compared to year-end filing?

Year-end tax filing is a compliance activity. Year-round tax planning is a profit strategy. The distinction matters because ongoing tax planning with real-time financial visibility tools produces measurably better outcomes than reactive, hindsight-based approaches.

The risks of relying solely on year-end filing are concrete:

- You cannot change your entity structure retroactively after the tax year closes.

- Retirement plan contributions must often be set up before year-end to count for that tax year.

- Income timing decisions, like delaying invoices or accelerating expenses, require advance planning.

- Estimated tax underpayments accumulate penalties that a quarterly review would have caught.

Proactive modeling for entity structure, income allocation, and state tax filings aligned with growth plans reduces surprises and improves tax strategy. Quarterly reviews are the minimum cadence for a firm generating over $500,000 in revenue. At that level, a single missed planning opportunity can cost more than a year of accounting fees.

The tools that make year-round planning practical include:

| Tool / Approach | Primary Benefit | Best For |

|---|---|---|

| Cloud accounting (QuickBooks, Xero) | Real-time P&L and cash flow visibility | All firm sizes |

| KPI dashboards | Tax liability forecasting tied to revenue | Firms over $500K revenue |

| Fractional CFO engagement | Scenario modeling and strategic tax decisions | Firms over $1M revenue |

| Quarterly tax reviews | Estimated tax accuracy and credit tracking | All firm sizes |

A fractional CFO adds particular value for professional service firms that are growing but not yet large enough to justify a full-time financial executive. The fractional model gives you access to scenario analysis, cash flow forecasting, and tax strategy coordination at a fraction of the cost. Truemeasureaccounting offers fractional CFO services specifically designed for owner-operated firms in this revenue range.

Accrual accounting offers better management insight than cash basis, even when cash basis is used for tax purposes. Running dual-method reporting, accrual for management decisions and cash for tax filing, gives you the clearest picture of both profitability and tax liability at the same time.

Key takeaways

Effective tax reduction for a professional service firm requires integrating entity structuring, compensation optimization, retirement plan design, and proactive credit documentation into a single, year-round strategy.

| Point | Details |

|---|---|

| Entity structure drives the largest savings | S-Corp election reduces self-employment tax on distributions; holding companies add further planning flexibility. |

| Compensation must be modeled annually | Reasonable salary, distributions, and retirement contributions interact; optimize all three together each year. |

| Retirement plans shelter the most income | Cash balance and defined benefit plans can shelter $100,000 to $300,000 annually for owners aged 50 and above. |

| Documentation determines credit eligibility | Project codes and real-time tagging in QuickBooks or Xero make R&D and energy credits defensible and claimable. |

| Year-round planning outperforms year-end filing | Quarterly reviews, scenario modeling, and fractional CFO support produce better outcomes than reactive compliance. |

What I’ve learned from watching owners leave money on the table

Most professional service firm owners I work with are sharp operators. They know their craft, they manage their teams well, and they price their services competitively. But when it comes to tax strategy, the majority are operating with a single point of contact, a CPA who files their return and maybe takes a call in November. That is not a strategy. That is compliance.

The owners who genuinely reduce their tax burden year after year share one habit: they treat tax planning as a business decision, not a paperwork obligation. They ask their CPA and their attorney to sit in the same room, or at least the same conversation. High-level tax optimization requires legal restructuring beyond what CPAs typically offer, and that interdisciplinary partnership is where the real savings live.

I have also seen how documentation discipline separates firms that claim credits from firms that qualify for them but cannot prove it. The R&D credit is a perfect example. Many consulting and engineering firms do qualifying work every single day. But because no one tagged the project codes or logged the time correctly, the credit is unclaimable. That is not a tax problem. That is an operations problem with a tax consequence.

My honest advice: stop waiting for your accountant to tell you what to do. Get a quarterly meeting on the calendar, bring your revenue projections, and ask specifically what decisions you need to make before year-end. The firms that do this consistently pay significantly less in taxes than those that do not. Not because they found a loophole, but because they planned ahead.

— Tony

How Truemeasureaccounting helps professional service firms reduce taxes

Truemeasureaccounting works with professional service firms across the country to implement the exact strategies covered in this guide. From entity structure analysis and compensation modeling to retirement plan coordination and real-time bookkeeping that supports credit documentation, the firm brings an operator’s perspective to every engagement.

Unlike traditional accounting firms focused on compliance, Truemeasureaccounting connects your financial data to real business decisions. Whether you need tax preparation and planning or ongoing bookkeeping services that keep your records credit-ready year-round, the team is built to support firms generating $250,000 to $5 million in annual revenue. Schedule a free consultation to see where your firm’s tax strategy has room to improve.

FAQ

What is the most effective way to reduce taxes for a professional service firm?

The most effective approach combines S-Corp entity structuring, reasonable compensation planning, and qualified retirement plan contributions. These three strategies together can reduce taxable income by $100,000 or more annually for a firm generating $500,000 or above.

How much can a cash balance plan reduce my taxable income?

Cash balance plans can shelter $60,000 to $300,000 or more from taxable income each year, depending on the owner’s age and income level. Owners aged 50 and above typically see the highest contribution limits and the greatest tax impact.

What tax credits do professional service firms commonly overlook?

The R&D tax credit, Section 179D energy efficiency deduction, and state-level job creation credits are the most frequently overlooked. Poor documentation is the primary reason eligible firms fail to claim them, not lack of qualifying activity.

How often should a professional service firm review its tax strategy?

Quarterly reviews are the minimum for firms generating over $500,000 in annual revenue. Waiting until year-end eliminates most planning opportunities, including entity elections, retirement plan setup deadlines, and income timing decisions.

Does an S-Corp always make sense for a professional service firm?

Not always. S-Corps work best when the owner’s reasonable salary is significantly lower than total firm profits. For firms with thin margins or owners who need to take most profits as salary, the payroll tax savings may not justify the added administrative complexity. Model the numbers before converting.