Depreciation is defined as the IRS-sanctioned method of recovering capital asset costs over multiple years rather than deducting the full purchase price in a single tax year. For trucking company owners and operators, understanding the role of depreciation in trucking business taxes is not optional. It directly determines how much taxable income you report, how much self-employment tax you owe, and whether a truck purchase actually improves your financial position after accounting for future recapture. The IRS governs every aspect of this process through rules covering MACRS schedules, Section 179 elections, and bonus depreciation. Getting it right means keeping significantly more money in your business.

What are the main depreciation methods used in trucking tax filings?

Trucking assets, including semi-trucks, trailers, and most heavy equipment, are classified as 5-year MACRS property under the Modified Accelerated Cost Recovery System. MACRS is the standard depreciation schedule the IRS requires for most business assets. Under the standard MACRS 5-year schedule, you spread deductions across six tax years due to the half-year convention, which assumes assets are placed in service at the midpoint of the year. This method is predictable but slow, and most trucking operators have better options available.

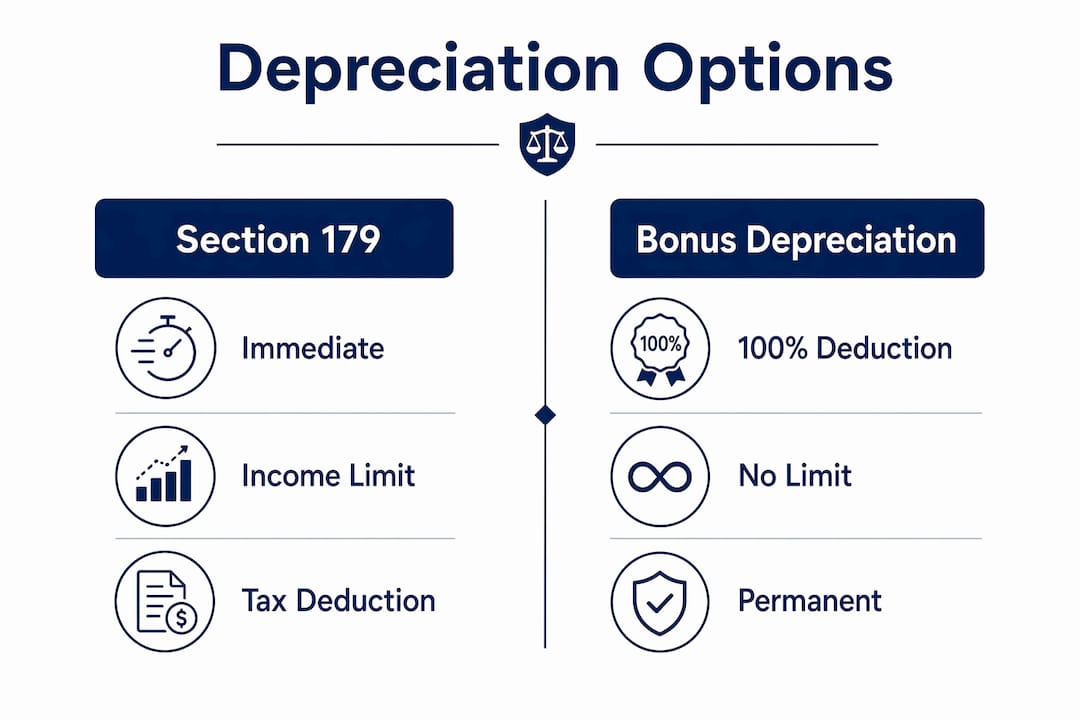

Section 179: immediate expensing with income limits

Section 179 lets you deduct the full cost of qualifying equipment in the year it is placed in service, up to the annual limit. The critical constraint is that Section 179 cannot exceed taxable income. If your trucking business shows $80,000 in net income before the deduction, your Section 179 election cannot push you into a net operating loss. Any unused deduction carries forward to future years, which limits its usefulness in low-income years.

Bonus depreciation: the more powerful tool in 2026

For property placed in service after January 19, 2025, 100% bonus depreciation permanently applies under the One Big Beautiful Bill framework. This means you can write off the entire cost of a qualifying truck or trailer in year one with no income cap. Unlike Section 179, bonus depreciation can generate a net operating loss that carries forward to offset future taxable income. That flexibility makes it the more powerful tool for operators with variable income or those making large equipment purchases.

Here is a side-by-side comparison of the three primary methods:

| Method | Income limit | Can create NOL? | Best use case |

|---|---|---|---|

| MACRS (standard) | None | No | Predictable, spread-out deductions |

| Section 179 | Capped at taxable income | No | High-income years, controlled deductions |

| Bonus depreciation | None | Yes | Large purchases, variable income years |

The practical impact is significant. A trucking company that buys a $150,000 semi-truck and elects 100% bonus depreciation eliminates $150,000 of taxable income in year one. At a combined federal and self-employment tax rate of roughly 35%, that represents over $52,000 in immediate tax savings. That is real cash staying in your operation.

Pro Tip: Apply Section 179 first to use up taxable income, then layer bonus depreciation on top for any remaining asset cost. This sequencing maximizes current-year deductions while preserving NOL carryforward potential for future planning.

Trucking expense write-offs extend beyond depreciation to include fuel, maintenance, insurance, and driver wages, but depreciation on capital assets typically produces the largest single-year deduction available to owner-operators. Understanding how depreciation affects taxes across all these categories is where real tax savings are built.

How does depreciation timing and recapture impact trucking business taxes?

Accelerated depreciation is a timing tool. It pulls deductions forward into the current tax year, reducing your bill now. But the IRS does not forget what you deducted. When you sell a truck for more than its adjusted tax basis, the gain up to the amount of prior depreciation is taxed as ordinary income under Section 1245. This is called depreciation recapture, and it catches many trucking operators off guard.

Here is how recapture works in a real scenario:

- You purchase a truck for $120,000 and take 100% bonus depreciation in year one. Your adjusted tax basis drops to $0.

- Three years later, you sell the truck for $60,000.

- The entire $60,000 gain is treated as ordinary income under Section 1245 recapture rules, not as a lower-taxed capital gain.

- At a 37% federal income tax rate, that sale generates a $22,200 tax bill you may not have planned for.

- The net tax benefit of the original deduction must now be weighed against this recapture cost when evaluating the true financial outcome.

Depreciation recapture under Section 1245 converts prior depreciation into ordinary income when trucks are sold above their adjusted basis. This is not a penalty. It is the IRS collecting deferred tax. The problem is that many operators take aggressive deductions in year one and then face a surprise tax bill when they trade in or sell equipment years later.

Acquisition and placed-in-service dates matter enormously. Bonus depreciation eligibility for the 100% rate is tied to specific post-January 19, 2025 acquisition and placed-in-service rules. A truck ordered in December 2024 but not delivered and placed in service until February 2025 may qualify under the new rules. Documentation of both dates is not optional. It is the difference between a full deduction and a phased one.

Depreciation is a tax timing tool, not a permanent tax elimination. Operators who model only the purchase-year savings without accounting for recapture at sale are working with an incomplete financial picture.

Pro Tip: Before selling any truck or trailer, ask your CPA to calculate the recapture tax exposure. In many cases, timing the sale to a lower-income year reduces the ordinary income tax rate applied to the recaptured amount, saving thousands.

The impact of depreciation on profits is most visible in year one, but the full picture only becomes clear when you track the asset from purchase through sale. That requires accurate bookkeeping from day one.

Ownership vs. leasing: which gives you better depreciation tax benefits?

The choice between owning and leasing a truck is fundamentally a tax decision as much as a financial one. Ownership enables depreciation deductions that reduce taxable income directly. An operating lease, by contrast, gives you deductible lease payments but zero depreciation claims. You never own the asset, so you never recover its cost through depreciation.

The tax treatment of lease-purchase agreements adds a layer of complexity. Most lease-purchase deals in trucking are treated as ownership for tax purposes, not as true operating leases. That means you can claim depreciation, but you also carry the recapture risk at the end of the agreement. Many owner-operators sign lease-purchase contracts believing they are getting the simplicity of a lease, only to discover they have the tax obligations of an owner.

Here is a direct comparison of the tax implications:

| Factor | Ownership | Operating lease |

|---|---|---|

| Depreciation deduction | Yes, full cost recovery | No |

| Lease payment deduction | No | Yes, fully deductible |

| Recapture risk at sale | Yes | No |

| Year-one tax savings potential | High (with bonus depreciation) | Moderate |

| Balance sheet impact | Asset recorded | Off-balance-sheet |

The cash flow impact is real. An owner-operator who buys a $150,000 truck and takes 100% bonus depreciation may owe no federal income tax in year one. An operator leasing the same truck at $2,500 per month deducts $30,000 annually. The ownership path produces far greater short-term tax savings, but it also creates future recapture exposure that the leasing path avoids entirely.

Key considerations when choosing between ownership and leasing:

- Income level: High-income years favor ownership with accelerated depreciation. Low-income years may favor leasing to preserve deductions for when they matter more.

- Truck turnover rate: Operators who trade trucks every two to three years face more frequent recapture events. Leasing may reduce that complexity.

- Cash position: Bonus depreciation reduces tax liability but does not replace cash. Lease payments are predictable and preserve working capital.

- Long-term plans: Operators building equity in their fleet benefit from ownership. Those prioritizing flexibility benefit from operating leases.

Diesel fuel costs and market conditions also affect this calculation. Understanding how market trends affect operating costs helps frame the total cost of ownership picture alongside depreciation tax benefits.

How to integrate depreciation into your trucking business tax strategy

Depreciation is most powerful when it is planned, not reactive. Most trucking operators make equipment purchases based on operational need and then figure out the tax treatment afterward. The smarter approach is to model the tax outcome before signing any purchase agreement.

Start by assessing your projected taxable income for the year before deciding between Section 179 and bonus depreciation. If your income is high and stable, Section 179 gives you a controlled deduction that does not create an NOL. If your income is variable or you expect a strong year followed by a weaker one, bonus depreciation with an NOL carryforward may produce better results across multiple years. Depreciation affects both income tax and self-employment tax for owner-operators, so every dollar of reduced net income has a compounding tax benefit.

Practical steps for building depreciation into your tax strategy:

- Time your purchases. Placing a truck in service before December 31 qualifies it for a full year of depreciation under most methods. A purchase delayed by one week can shift a major deduction into the next tax year.

- Track your basis. Every improvement, major repair, or addition to a truck affects its tax basis. Accurate records prevent errors on depreciation schedules and reduce recapture surprises at sale.

- Model the full lifecycle. A CPA should run the numbers from purchase through projected sale, including recapture tax, to determine the true after-tax cost of ownership.

- Use NOL carryforwards wisely. Bonus depreciation can generate a net operating loss that carries forward indefinitely under current tax law. Plan which future year absorbs that loss for maximum benefit.

- Avoid the common timing mistake. Many operators place trucks in service late in Q4 without realizing the mid-quarter convention applies if more than 40% of depreciable assets are placed in service in the final quarter. This can reduce first-year deductions significantly.

Pro Tip: If you are planning a major truck purchase in Q4, consult your accountant before October 1. The mid-quarter convention can cut your first-year MACRS deduction by more than half if you are not careful. Bonus depreciation sidesteps this issue entirely, which is another reason it is often the better election.

Tax strategies for trucking companies that incorporate depreciation planning at the beginning of the year, not at tax time, consistently produce better outcomes. Depreciation is not a year-end tax trick. It is a year-round financial planning tool.

Key takeaways

Depreciation in trucking business taxes is a timing strategy that reduces current taxable income but creates recapture obligations at sale, requiring full lifecycle planning to maximize its true financial benefit.

| Point | Details |

|---|---|

| Depreciation defined | The IRS requires cost recovery over multiple years; one-time deductions are not permitted for capital assets. |

| Bonus depreciation in 2026 | 100% first-year expensing applies permanently for qualifying assets placed in service after January 19, 2025. |

| Section 179 vs. bonus depreciation | Section 179 is capped by taxable income; bonus depreciation has no cap and can generate an NOL carryforward. |

| Recapture risk is real | Selling a truck above its adjusted basis triggers ordinary income tax on prior depreciation under Section 1245. |

| Ownership vs. leasing | Ownership enables depreciation deductions; operating leases provide payment deductions but no cost recovery. |

What I have learned about depreciation after years of working with trucking businesses

Every trucking operator I have worked with initially views depreciation as a straightforward tax win. Buy a truck, write it off, pay less tax. That framing is not wrong, but it is incomplete. The operators who get into trouble are the ones who optimize for year-one savings without thinking about what happens in year three or four when that truck gets sold or traded.

I have seen owner-operators take 100% bonus depreciation on a $200,000 truck, reduce their tax bill to near zero, and then face a $50,000 tax bill two years later when they sold the truck for $90,000. They had not planned for recapture. The money they saved in year one was already spent on operations. The recapture bill felt like it came out of nowhere, but it was always there in the math.

The other pattern I see constantly is operators who choose between Section 179 and bonus depreciation based on what their tax preparer suggests at filing time, with no forward-looking modeling. That is the wrong sequence. The decision about how to depreciate a truck should happen before you buy it, not after. You need to know your projected income, your expected holding period, and your likely sale price to make an informed election.

What actually works is treating depreciation as one piece of a multi-year tax plan. That means tracking your basis accurately in QuickBooks or whatever accounting system you use, running recapture projections before every sale, and timing purchases with your income cycle in mind. It also means understanding that depreciation is a timing tool, not a permanent tax reduction. The IRS will collect eventually. Your job is to control when and how much.

The trucking operators who build real financial clarity around depreciation are the ones who stop reacting to tax bills and start planning around them. That shift from reactive to proactive is where the real financial gains live.

— Tony

How TrueMeasure Accounting helps trucking businesses manage depreciation

Depreciation planning is one of the highest-value services we provide to trucking clients at TrueMeasure Accounting. We do not just record what happened. We model what is coming.

Our team works directly with trucking company owners and owner-operators to build depreciation schedules, run recapture projections, and time equipment purchases for maximum tax benefit. We connect your trucking bookkeeping services to a proactive tax strategy so you are never surprised at filing time. Whether you need QuickBooks cleanup, tax preparation, or fractional CFO support, our small business bookkeeping services are built for operators like you. Contact TrueMeasure Accounting today to schedule a consultation and take control of your depreciation strategy before your next purchase.

FAQ

What is the role of depreciation in trucking business taxes?

Depreciation allows trucking businesses to recover the cost of trucks, trailers, and equipment over time, reducing taxable income each year rather than taking a single deduction. The IRS requires this cost recovery method for all capital assets used in business operations.

How does bonus depreciation work for trucking companies in 2026?

For qualifying assets placed in service after January 19, 2025, 100% bonus depreciation applies permanently, allowing trucking operators to deduct the full cost of a truck in the year it is placed in service. Unlike Section 179, bonus depreciation has no income cap and can generate a net operating loss that carries forward.

What is depreciation recapture and how does it affect trucking operators?

Depreciation recapture under Section 1245 taxes the gain on a truck sale, up to the amount of prior depreciation taken, as ordinary income rather than capital gains. Operators who took 100% bonus depreciation and later sell the truck above its $0 adjusted basis will owe ordinary income tax on the full sale price.

Should a trucking company own or lease trucks for better tax benefits?

Ownership enables depreciation deductions that can eliminate taxable income in year one, while operating leases only allow deduction of lease payments with no depreciation. High-income operators with stable cash flow typically benefit more from ownership, while operators prioritizing flexibility may prefer leasing.

How can trucking operators avoid common depreciation mistakes?

The most common mistakes are failing to document placed-in-service dates, ignoring the mid-quarter convention in Q4 purchases, and not modeling recapture tax before selling equipment. Working with a CPA who understands trucking tax deductions and depreciation schedules prevents these costly errors.

Recommended

- Types of Trucking Business Expenses to Track in 2026

- How Truck Drivers Can Maximize Tax Deductions (and Save 1000s) – TrueMeasure Accounting LLC-Small Business Accounting Services

- Truckers financial services: Helping Truckers Navigate 2025 Trend – TrueMeasure Accounting LLC-Small Business Accounting Services

- Are You Pricing Your Trucking and Moving Services Right in 2025? – TrueMeasure Accounting LLC-Small Business Accounting Services